Logan Energy Corp. Announces Strategic Montney Asset Acquisition, $50.0 Million in Equity Offerings, Expanded Credit Facilities and Pro Forma Guidance for 2026

NOT FOR DISTRIBUTION TO U.S. NEWS WIRE SERVICES OR DISSEMINATION IN THE UNITED STATES. ANY FAILURE TO COMPLY WITH THIS RESTRICTION MAY CONSTITUTE A VIOLATION OF U.S. SECURITIES LAW.

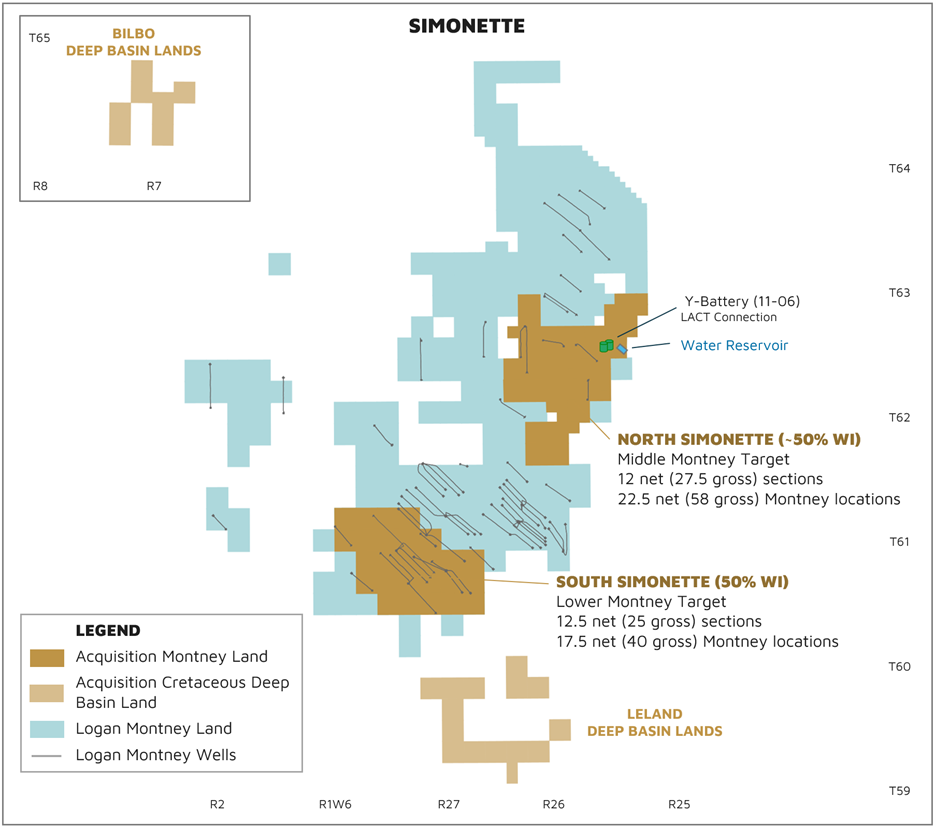

CALGARY, Alberta, Feb. 19, 2026 (GLOBE NEWSWIRE) -- Logan Energy Corp. (TSXV: LGN) ("Logan" or the "Company") is pleased to announce that it has entered into a definitive purchase agreement today with a subsidiary of a publicly-traded oil and gas company (the "Vendor"), pursuant to which Logan will acquire the Vendor's entire interest in certain assets predominantly in the Company’s core area at Simonette, Alberta (the "Acquired Assets") for cash consideration of $62.5 million, prior to closing adjustments (the “Acquisition”). The Acquisition has an effective date of January 1, 2026, and is expected to close on or around March 10, 2026 (the "Closing Date"), subject to the satisfaction or waiver of customary closing conditions.

Logan previously acquired a 50% operated working interest in certain Simonette assets from the Vendor on December 17, 2024. The Acquisition strategically consolidates these Montney-focused joint interest partner lands to a 100% working interest and includes incremental Deep Basin lands offsetting Simonette in the Bilbo and Leland areas of Alberta. The Acquisition is highly accretive on all key metrics both immediately and in the long term, significantly enhancing Logan’s long term organic growth plan.

Logan is also pleased to announce concurrent bought deal equity financings for aggregate gross proceeds of $50.0 million and an expansion of the Company’s revolving credit facilities to $250.0 million.

ACQUISITION HIGHLIGHTS

- The Acquisition includes current production of approximately 1,400 BOE/d (59% liquids), 24.5 net (52.5 gross) sections of highly prospective Montney acreage with 40 net identified Montney drilling locations at a cost of $0.6 million per location (1).

- Consideration of $62.5 million is approximately 2.2x 2026E Operating Income (at US$60/bbl WTI and C$3.00/GJ AECO).

- Consideration relative to the Acquired Assets YE2025 reserve values are 1.6x PDP, 0.6x TP and 0.4x TPP (BTax NPV10). The Acquisition will increase Logan’s reserve values across categories by 15% to 19% relative to 10% dilution (on a fully diluted basis) from the Equity Offerings (as defined herein). Pro forma the Acquisition, Logan’s reserve TP NAV will increase to $0.75 per fully diluted share and TPP NAV to $1.45 per fully diluted share (2)(6).

- Annualized AFF per share (as defined herein) accretion exceeds 5% in 2026 and 10% in 2027, respectively, and continues to demonstrate strong per share accretion over Logan’s long term organic growth plan.

- Financing structure is approximately leverage neutral relative to Logan’s pre-Acquisition 2026 budget.

- Acquisition adds top tier Alberta Montney oil inventory; South Simonette Lower Montney oil wells are delivering a booked TPP oil EUR of 475mbbl of oil with an NPV10 of $12.7 million (YE2025 pricing) (3)(6).

- Additional development opportunities in Cretaceous Deep Basin horizons with 10.2 net identified undeveloped locations (4).

- Since the initial 2024 acquisition for $62.7 million (inclusive of closing adjustments and capital obligations), the Vendor’s working interest share of PDP reserves in Simonette have increased in value from $6.6 million to $40.3 million (BTax NPV10) (5)(6).

Notes: Refer to “Reader Advisories”.

ACQUISITION METRICS

| Purchase Price (1) | $62.5MM |

| February 2026 Production (2) | 1,400 BOE/d (59% liquids) |

| Next Twelve Months Production (Forecast) (3) | 2,100 BOE/d (64% liquids) |

| Next Twelve Months Operating Netback (Forecast) (4) | $40.81 / BOE |

| Next Twelve Months Operating Income (Forecast) (4) | $31MM |

| Montney Drilling Locations – booked (5) | 40 gross (18.6 net) |

| Montney Drilling Locations – unbooked (5) | 58 gross (21.7 net) |

| Reserve Volumes (6) Proved Developed Producing (“PDP”) Total Proved (“TP”) Total Proved plus Probable (“TPP”) |

2,406 mBOE 8,277 mBOE 15,863 mBOE |

| Reserve Values (before-tax NPV at 10%) (6) (7) PDP TP TPP |

$40.3MM $97.8MM $167.7MM |

| Decommissioning Obligations (Undiscounted) (8) | ~ $17.6MM |

Notes: Refer to “Reader Advisories”.

EQUITY OFFERINGS

Logan has entered into an agreement with a syndicate of underwriters (the "Underwriters") co-led by National Bank Capital Markets as sole bookrunner and co-lead underwriter, and TD Securities Inc. as co-lead underwriter, pursuant to which the Underwriters have agreed to purchase for resale an aggregate of 68,494,000 common shares ("Common Shares") of Logan at a price of $0.73 per Common Share (the “Issue Price”) for gross proceeds of $50.0 million (the "Equity Offerings"). The Equity Offerings will be conducted, on a bought deal basis, by way of a public offering of 34,247,000 Common Shares at the Issue Price (the "Prospectus Offering") and a private placement of 34,247,000 Common Shares at the Issue Price (the "Private Placement").

Closing of the Equity Offerings will be conditional on the completion of the Acquisition in accordance with the terms of an asset purchase agreement between Logan and the Vendor dated February 19, 2026, in respect of the Acquisition. Logan intends to use the net proceeds from the Equity Offerings to repay indebtedness incurred to fund a portion of the purchase price for the Acquisition. The completion of the Equity Offerings is also subject to customary closing conditions, including the receipt of all necessary regulatory approvals, including the approval of the TSX Venture Exchange ("TSXV"). Closing of the Equity Offerings is expected to occur immediately following closing of the Acquisition on March 10, 2026.

The Underwriters have been granted an option to purchase up to an additional 15% of the Common Shares issued under the Prospectus Offering at the Issue Price to cover over allotments exercisable in whole or in part at any time until 30 days after the closing of the Prospectus Offering.

The Common Shares offered in the Prospectus Offering will be offered by way of short form prospectus in all provinces of Canada except Québec. The Common Shares may also be placed privately in the United States to Qualified Institutional Buyers (as defined under Rule 144A under the United States Securities Act of 1933, as amended (the "U.S. Securities Act")), pursuant to an exemption under Rule 144A, and may be distributed outside Canada and the United States on a basis which does not require the qualification or registration of any of the Company’s securities under domestic or foreign securities laws. The Common Shares issued under the Private Placement will be issued on a private placement basis only and will be subject to a statutory hold period that extends four months plus one day from the Closing Date of the Private Placement.

The Company has agreed to pay a cash commission of 4.0% of the gross proceeds of the Equity Offerings to the Underwriters. It is anticipated that certain directors, officers and employees of the Company will subscribe for approximately $2.0 million of the Private Placement.

INCREASE TO CREDIT FACILITY

Logan is pleased to announce it has received a $250.0 million commitment from National Bank Capital Markets for increased credit facilities. Closing of the expanded credit facilities will be concurrent with the Acquisition on the Closing Date.

ADVISORS

National Bank Capital Markets is acting as financial advisor to Logan in respect of the Equity Offerings and the expanded credit facilities. TD Securities Inc. is acting as strategic advisor to Logan in respect of the Acquisition.

Stikeman Elliott LLP is acting as legal counsel to Logan in respect of the Acquisition, the Equity Offerings and the expanded credit facilities.

Burnet, Duckworth & Palmer LLP is acting as legal counsel to the Underwriters in respect of the Equity Offerings.

PRO FORMA 2026 GUIDANCE AND UPDATED OPERATING PLAN

Logan has updated its guidance for 2026 to reflect the Acquisition and Equity Offerings, including an expanded budget for Capital Expenditures before A&D of $175-185 million (previously $140-150 million) and increased average production guidance for 2026 by 6% to 16,000-17,000 BOE/d (previously 15,000-16,000 BOE/d).

The expanded capital budget reflects the incremental capital on the joint Acquired Assets increasing from 50% to 100% working interest, as well an activity re-allocation on Logan’s existing assets. On Logan’s existing assets, Logan plans to reduce one Montney well planned in Pouce Coupe to balance capital spending levels.

Logan is also now budgeting and planning to complete its first delineation well in Flatrock in late 2026, subject to commodity prices. Flatrock represents a high impact Montney development opportunity with scale and the expected reservoir attributes to deliver highly economic Montney oil and gas wells. Logan is excited to demonstrate this asset’s potential with anticipated results in 2026. With success, Logan has identified over 240 Montney locations in Flatrock.

| For the year ending December 31, 2026 |

Previous Guidance (1) |

Updated Guidance (1) |

Change |

% |

| 2026 average production (BOE/d) (2) | 15,000 - 16,000 | 16,000 - 17,000 | 1,000 | 6 |

| % Liquids | 39% | 42% | 3% | 8 |

| H2 2026 average production (BOE/d) (2) | 16,500 - 17,500 | 18,000 - 19,000 | 1,500 | 9 |

| % Liquids | 41% | 44% | 3% | 7 |

| Forecast Average Commodity Prices (3) | ||||

| WTI crude oil price (US$/bbl) | 60.00 | 60.00 | - | - |

| AECO natural gas price ($/GJ) | 3.00 | 3.00 | - | - |

| Average exchange rate (CA$/US$) | 1.40 | 1.40 | - | - |

| Operating Netback, after hedging ($/BOE) (2)(3)(4) | 25.35 | 27.07 | 1.72 | 7 |

| Adjusted Funds Flow ($MM) (2)(4) | 120 | 138 | 18 | 15 |

| AFF per share, basic (2)(4)(5) | 0.20 | 0.21 | 0.01 | 5 |

| Capital Expenditures before A&D ($MM) (2) | 140 - 150 | 175 – 185 | 35 | 24 |

| Acquisitions (6) | - | 66 | 66 | nm |

| Net Debt, end of year ($MM) (4) | 116 | 149 | 33 | 28 |

| Common shares outstanding, end of year (MM) (5) | 596 | 664 | 68 | 11 |

| (1) | The financial performance measures included in the Company’s guidance for 2026 are based on the midpoint of the average production and capital expenditure forecast. Previous guidance for 2026 was published in the Company’s press release dated January 5, 2026. |

| (2) | Additional information regarding the assumptions used in the forecasts of average production, Operating Netback and Adjusted Funds Flow are provided under "Reader Advisories" below. |

| (3) | A summary of outstanding commodity price risk management contracts is provided under the heading "Reader Advisories - Assumptions for Guidance – Commodity Hedging". |

| (4) | "Operating Netback, after hedging", "Adjusted Funds Flow", "AFF per share", "Capital Expenditures before A&D" and "Net Debt (Surplus)" do not have standardized meanings under IFRS Accounting Standards, see "Non-GAAP Measures and Ratios" section of this press release. |

| (5) | The forecast of basic Common Shares outstanding assumes closing of the Equity Offerings for aggregate gross proceeds of $50.0 million. AFF per share is based on the estimated basic weighted average common shares outstanding during the year. Refer to additional information regarding outstanding dilutive securities under the heading "Share Capital" in this press release. |

| (6) | Includes the $62.5 million purchase price for the Acquisition plus $3.2 million of estimated closing adjustments. |

ABOUT LOGAN ENERGY CORP.

Logan is a growth-oriented exploration, development and production company formed through the spin-out of the early stage Montney assets of Spartan Delta Corp. Logan has three high quality and opportunity rich Montney assets located in the Simonette and Pouce Coupe areas of northwest Alberta and the Flatrock area of northeastern British Columbia. Additionally, the Company has established a position within the greater Kaybob Duvernay oil play with assets in the North Simonette, Ante Creek and Two Creeks areas. The management team brings proven leadership and a track record of generating excess returns in various business cycles.

For additional information, please contact:

| Richard F. McHardy | Logan Energy Corp. |

| Chief Executive Officer | 900, 355 – 4th Avenue SW |

| Calgary, Alberta T2P 0J1 | |

| Brendan Paton | Email: info@loganenergycorp.com |

| President and Chief Operating Officer | https://www.loganenergycorp.com/ |

READER ADVISORIES

|

Notes to Acquisition Highlights: | |

| 1) | Of the 40 net (98 gross) identified Montney locations, there are 40 gross (18.6 net) booked locations in the Reserves Report with an additional 58 gross (21.7 net) unbooked locations identified by Logan. See “Drilling Locations” for additional details. Cost per location is calculated as total consideration less $40.3 million PDP NPV10 BTax reserve value divided by 40 net locations. Field estimated average production for February 2026 from the Acquired Assets is approximately 1,400 BOE/d, consisting of 770 bbl/d of oil (55%), 56 bbl/d of NGLs (4%), and 3,444mcf/d of natural gas (41%). |

| 2) | See “Reserves Disclosure” for additional details. |

| 3) | South Simonette Lower Montney oil wells as evaluated in the Reserves Report. |

| 4) | 10.2 net (20 gross) identified locations are unbooked; See “Drilling Locations” for additional details. |

| 5) | See Logan’s press release dated November 26, 2024 for details of the PDP reserves at the time of the initial 2024 acquisition. See “Reserves Disclosure” for additional details relating to the PDP reserves attributed to this acquisition. |

| 6) | The estimates of reserves and future net revenue for individual properties may not reflect the same confidence level as estimates of reserves and future net revenue for all properties, due to the effects of aggregation. |

|

Notes to Acquisition Metrics table: | |

| 1) | The purchase price to be paid by Logan in respect of the Acquisition is $62.5 million in cash, before closing adjustments. The Company expects purchase price adjustments, which include estimated cash flows and capital expenditures between the effective date of January 1, 2026 and the Closing Date, to be approximately $3.2 million in favour of the Vendor due to capital expenditures on recent drilling activity. Total consideration inclusive of closing adjustments is estimated to be approximately $65.7 million. |

| 2) | See Note (1) above in “Notes to the Acquisition Highlights” for BOE per day composition. |

| 3) | Average production forecast for the Acquired Assets over the next twelve months following closing is approximately 2,100 BOE/d, consisting of 1,266 bbl/d of oil (61%), 72 bbl/d of NGLs (3%), and 4,577 MMcf/d of natural gas (36%). |

| 4) | 2026 Operating Netback and Operating Income forecast based on commodity price assumptions of US$60/bbl WTI and $3.00/GJ AECO. Operating Income and Operating Netback are non-GAAP measures. See "Non-GAAP Measures and Ratios" for additional details. |

| 5) | See Note (1) above in “Notes to the Acquisition Highlights” for details on drilling locations. |

| 6) | Reserve volumes and values were derived from the Reserves Report and mechanically updated by Logan’s management. Reserves volumes and values are based on working interest reserves of the Acquired Assets before deduction of royalties and without including any of royalty interest reserves. See “Reserves Disclosure” for additional details. • PDP consisting of 1.1 MMbbl of crude oil (45%), 0.1 MMbbl of NGLs (5%), and 7,280 MMcf of natural gas (50%). • TP consisting of 4.2 MMbbl of oil (52%), 0.3 MMbbl of NGLs (3%), and 22,512 MMcf of natural gas (45%). • TPP consisting of 8.1 MMbbl of oil (51%), 0.5 MMbbl of NGLs (3%), and 43,535 MMcf of natural gas (46%). |

| 7) | Future development capital of $114.1 million net TP and $205.0 million net TPP are attributable to the Acquired Assets. |

| 8) | Decommissioning obligations for the Acquired Assets of approximately $17.6 million (undiscounted and uninflated) are internally estimated by Logan based on AER Directive 11 updates effective August 19, 2025 as well as internal estimate of reclamation costs and site specific information. |

Non-GAAP Measures and Ratios

This press release contains certain financial measures and ratios which do not have standardized meanings prescribed by International Financial Reporting Standards as issued by the International Accounting Standards Board ("IFRS Accounting Standards"), also known as Canadian Generally Accepted Accounting Principles ("GAAP"). As these non-GAAP financial measures and ratios are commonly used in the oil and gas industry, Logan believes that their inclusion is useful to investors. The reader is cautioned that these amounts may not be directly comparable to measures for other companies where similar terminology is used.

The non-GAAP measures and ratios used in this press release, represented by the capitalized and defined terms outlined below, are used by Logan as key measures of financial performance and are not intended to represent operating profits nor should they be viewed as an alternative to cash provided by operating activities, net income or other measures of financial performance calculated in accordance with IFRS Accounting Standards.

The definitions below should be read in conjunction with the “Non-GAAP and Other Financial Measures” section of the Company’s MD&A dated November 12, 2025, which includes discussion of the purpose and composition of the specified financial measures and detailed reconciliations to the most directly comparable GAAP financial measures.

Operating Income and Operating Netback

Operating Income, a non-GAAP financial measure, is a useful supplemental measure that provides an indication of the Company's ability to generate cash from field operations, prior to administrative overhead, financing and other business expenses. "Operating Income, before hedging" is calculated by Logan as oil and gas sales, net of royalties, plus processing and other revenue, less operating and transportation expenses. “Operating Income, after hedging” is calculated by adjusting Operating Income, before hedging for realized gains or losses on derivative financial instruments.

The Company refers to Operating Income expressed per unit of production as an "Operating Netback" and reports the Operating Netback before and after hedging, both of which are non-GAAP financial ratios. Logan considers Operating Netback an important measure to evaluate its operational performance as it demonstrates its field level profitability relative to current commodity prices.

Adjusted Funds Flow

Cash provided by operating activities is the most directly comparable measure to Adjusted Funds Flow. "Adjusted Funds Flow" is reconciled to cash provided by operating activities by excluding changes in non-cash working capital, adding back transaction costs on acquisitions (if applicable). The Company utilizes Adjusted Funds Flow as a key performance measure in the Company's annual financial forecasts and public guidance.

The Company refers to Adjusted Funds Flow expressed per unit of production as an "Adjusted Funds Flow Netback".

Adjusted Funds Flow per share ("AFF per share")

AFF per share is a non-GAAP financial ratio used by the Logan as a key performance indicator. The basic and/or diluted weighted average Common Shares outstanding used in the calculation of AFF per share is calculated using the same methodology as net income per share.

Capital Expenditures before A&D

"Capital Expenditures before A&D" is used by the Company to measure its capital investment level compared to the Company's annual budgeted capital expenditures for its organic drilling program. It includes capital expenditures on exploration and evaluation assets and property, plant and equipment, before acquisitions and dispositions. The directly comparable GAAP measure to capital expenditures is cash used in investing activities.

Net Debt (Surplus)

Throughout this press release, references to “Net Debt” or “Net Surplus” includes bank debt, net of “Adjusted Working Capital”. Net Debt and Adjusted Working Capital are both non-GAAP financial measures. Adjusted Working Capital is calculated as current liabilities less current assets, excluding derivative financial instrument assets and liabilities and provisions and other liabilities. As of the date hereof, Adjusted Working Capital includes cash and cash equivalents, accounts receivable, prepaids and deposits, and accounts payable and accrued liabilities.

Supplementary Financial Measures

The supplementary financial measures used in this press release (primarily average sales price per product type and certain per BOE and per share figures) are either a per unit disclosure of a corresponding GAAP measure, or a component of a corresponding GAAP measure, presented in the financial statements. Supplementary financial measures that are disclosed on a per unit basis are calculated by dividing the aggregate GAAP measure (or component thereof) by the applicable unit for the period. Supplementary financial measures that are disclosed on a component basis of a corresponding GAAP measure are a granular representation of a financial statement line item and are determined in accordance with GAAP.

Assumptions for Guidance

The significant assumptions used in the forecast of Operating Netbacks and Adjusted Funds Flow for the Company’s pro forma 2026 guidance are summarized below.

| Production Guidance | 2026 Previous Guidance(1) |

2026 Pro Forma Guidance(1) |

Change % | |||

| Crude Oil (bbls/d) | 4,518 - 4,820 | 5,409 - 5,746 | 19 | |||

| Condensate (bbls/d) | 303 - 322 | 272 - 290 | (10 | ) | ||

| Crude oil and condensate (bbls/d) | 4,821 - 5,142 | 5,681 - 6,036 | 18 | |||

| NGLs (bbls/d) | 960 - 1,024 | 1,003 - 1,065 | 4 | |||

| Natural gas (mcf/d) | 55,313 - 59,001 | 55,898 - 59,392 | 1 | |||

| Combined average (BOE/d) | 15,000 - 16,000 | 16,000 - 17,000 | 6 | |||

| % Liquids | 39 | % | 42 | % | 8 | |

|

Financial Guidance ($/BOE) |

||||||

| Oil and gas sales | 39.20 | 41.22 | 5 | |||

| Processing and other revenue | 0.37 | 0.22 | (41 | ) | ||

| Royalties | (3.31 | ) | (3.53 | ) | 7 | |

| Transportation expenses | (2.25 | ) | (2.01 | ) | (11 | ) |

| Operating expenses | (8.75 | ) | (8.84 | ) | 1 | |

| Operating Netback, before hedging | 25.26 | 27.06 | 7 | |||

| Realized gain on derivatives | 0.09 | 0.01 | (89 | ) | ||

| Operating Netback, after hedging | 25.35 | 27.07 | 7 | |||

| General and administrative expenses | (1.68 | ) | (1.38 | ) | (18 | ) |

| Financing expenses | (2.18 | ) | (2.47 | ) | 13 | |

| Decommissioning obligations | (0.30 | ) | (0.28 | ) | (7 | ) |

| Adjusted Funds Flow | 21.19 | 22.94 | 8 | |||

| (1) | The financial performance measures included in the Company’s guidance for 2026 are based on the midpoint of the average production and capital expenditure forecast. |

Planned Activity

| Area |

Net (Gross) Wells Drilled(1) |

Net (Gross) Wells Completed(1) |

Net (Gross) Wells Onstream(1) |

| Simonette | 5 (5) | 5.7 (6) | 5.7 (6) |

| Pouce Coupe | 8 | 8 | 8 |

| Flatrock | - | 1 | - |

| (1) | Net and gross well counts are the same if not otherwise noted. |

Guidance Sensitivities

Changes in forecast commodity prices, exchange rates, differences in the amount and timing of capital expenditures, and variances in average production estimates can have a significant impact on the key performance measures included in Logan's pro forma guidance for 2026. The Company's actual results may differ materially from these estimates. Holding all other assumptions constant, the table below shows the impact to forecasted Adjusted Funds Flow of a US$5/bbl change in the WTI crude oil price, a $0.25/GJ change in the AECO natural gas price, and a $0.01 change in the CA$/US$ exchange rate. Assuming capital expenditures are unchanged, an increase (decrease) in Adjusted Funds Flow will result in an equivalent decrease (increase) in forecasted Net Debt.

| Year Ending December 31, 2026 – Change in Adjusted Funds Flow ($MM) | ||||||

| AECO / WTI | US$55.00/bbl | US$60.00/bbl | US$65.00/bbl | CA$/US$ | FX Impact | |

| $2.75/GJ | ($9) | ($3) | $3 | 1.39 | ($1) | |

| $3.00/GJ | ($6) | - | $6 | 1.40 | - | |

| $3.25/GJ | ($4) | $3 | $9 | 1.41 | $1 | |

Commodity Hedging

The following table summarizes the Company's financial risk management contracts in place as of the date hereof:

|

Commodity / Contract Type |

Notional Volume |

Reference Price |

Fixed Contract Price |

Remaining Term |

| Crude oil – swap | 3,000 bbls/d | WTI | CA$84.55 per barrel | February 1 to June 30, 2026 |

| Crude oil – swap | 3,000 bbls/d | WTI | CA$83.63 per barrel | July 1 to December 31, 2026 |

| Natural gas – swap | 28,500 GJ/d | AECO | CA$3.06 per GJ | February 1 to March 31, 2026 |

| Natural gas – swap | 30,000 GJ/d | AECO | CA$2.82 per GJ | April 1 to October 31, 2026 |

| Natural gas – swap | 30,000 GJ/d | AECO | CA$3.50 per GJ | November 1, 2026 to March 31, 2027 |

| Natural gas – swap | 15,000 GJ/d | AECO | CA$2.64 per GJ | April 1, 2027 to October 31, 2027 |

| Natural gas – swap | 10,000 GJ/d | AECO | CA$3.33 per GJ | November 1, 2027 to March 31, 2028 |

Reserves Disclosure

All reserves values, future net revenue and ancillary information in this press release relating to the Acquired Assets were derived from the oil and gas reserves evaluation with a preparation date of February 17, 2026 and as of December 31, 2025 as prepared by the Company's independent qualified reserves evaluator, McDaniel & Associates Consultants Ltd. (the "Reserves Report"), and mechanically updated by Logan’s management, in accordance with the definitions, standards and procedures contained in National Instrument 51-101 – Standards of Disclosure of Oil and Gas Activities ("NI 51-101") and the most recent publication of the Canadian Oil and Gas Evaluations Handbook ("COGEH"). The adjustments to the Reserves Report include carving out the Acquired Assets (reflective of the interest being acquired), adjusting the processing fees for Logan’s cost structure as an infrastructure owner and adding asset retirement obligation costs for the Acquired Assets. Additional information in respect of the Reserves Report is included in Logan’s press release dated February 17, 2026.

All reserve references in this press release are "gross reserves". Gross reserves are a company's total working interest reserves before the deduction of any royalties payable by such company and before the consideration of such company's royalty interests. It should not be assumed that the present worth of estimated future cash flow of net revenue presented herein represents the fair market value of the reserves. There is no assurance that the forecast prices and costs assumptions will be attained and variances could be material. The recovery and reserve estimates of Logan's crude oil, NGL and natural gas reserves, including those of the Acquired Assets, provided herein are estimates only and there is no guarantee that the estimated reserves will be recovered. Actual crude oil, natural gas and NGL reserves may be greater than or less than the estimates provided herein.

Proved reserves are those reserves that can be estimated with a high degree of certainty to be recoverable. It is likely that the actual remaining quantities recovered will exceed the estimated proved reserves. Probable reserves are those additional reserves that are less certain to be recovered than proved reserves. It is equally likely that the actual remaining quantities recovered will be greater or less than the sum of the estimated proved plus probable reserves. Proved developed producing reserves are those reserves that are expected to be recovered from completion intervals open at the time of the estimate. These reserves may be currently producing or, if shut-in, they must have previously been on production, and the date of resumption of production must be known with reasonable certainty. Undeveloped reserves are those reserves expected to be recovered from known accumulations where a significant expenditure (e.g., when compared to the cost of drilling a well) is required to render them capable of production. They must fully meet the requirements of the reserves category (proved, probable, possible) to which they are assigned. Certain terms used in this press release but not defined are defined in NI 51-101, CSA Staff Notice 51-324 – Revised Glossary to NI 51-101 ("CSA Staff Notice 51-324") and/or the COGEH and, unless the context otherwise requires, shall have the same meanings herein as in NI 51-101, CSA Staff Notice 51-324 and the COGEH, as the case may be.

Reserve values are based on the forecasted future prices that McDaniel used in their evaluation of the Company's reserves at December 31, 2025, which are based on a three-consultant average price forecast. The forecast cost and price assumptions assume increases in wellhead selling prices and consider inflation with respect to future operating and capital costs.

Drilling Locations

This press release discloses drilling locations with respect to the Acquired Assets in two categories: (i) booked; (ii) unbooked locations. Booked locations identified in this press release have associated proved and/or probable locations, as applicable, and proved and probable locations were derived from the Reserves Report in accordance with NI 51-101 and COGEH. Unbooked locations are internal estimates based on the Company's assumptions as to the number of wells that can be drilled per section based on industry practice and internal review, being 300 to 400m inter well spacing and an average horizontal well length of ~3,000m. Unbooked locations do not have attributed reserves or resources. Unbooked locations have been identified by management as an estimation of Logan's multi-year drilling activities based on evaluation of applicable geologic, seismic, engineering, production and reserves information. There is no certainty that the Company will drill all unbooked drilling locations and if drilled there is no certainty that such locations will result in additional oil and gas reserves, resources or production. The drilling locations on which the Company actually drills wells will ultimately depend upon the availability of capital, regulatory approvals, seasonal restrictions, oil and natural gas prices, costs, actual drilling results, additional reservoir information that is obtained and other factors. While certain of the unbooked drilling locations have been de-risked by drilling existing wells in relative close proximity to such unbooked drilling locations, the majority of other unbooked drilling locations are farther away from existing wells where management has less information about the characteristics of the reservoir and therefore there is more uncertainty whether wells will be drilled in such locations and if drilled there is more uncertainty that such wells will result in additional oil and gas reserves, resources or production.

Net Asset Value

The components of Logan’s “Net Asset Value” calculation set-forth in the table below. The reader is cautioned that these amounts may not be directly comparable to other companies, as the term Net Asset Value does not have a standardized meaning under IFRS Accounting Standards or NI 51-101. The NPV of reserves was determined by McDaniel in their year-end evaluation reports, based on a discount rate of 10% before-tax.

| NET ASSET VALUE | December 31, 2025 – Pro Forma | |||

| ($ millions, except per share amounts) | TP | TPP | ||

| NPV of reserves, discounted at 10% before tax (1) | 630 | 1,151 | ||

| Less: Net Debt [unaudited] (2) | (103 | ) | (103 | ) |

| Proceeds from exercise of options & warrants (3)(4) | 36 | 36 | ||

| Net asset value | 563 | 1,084 | ||

| Fully diluted common shares outstanding (MM) (3)(4)(5) | 748 | 748 | ||

| Net asset value ($ per common share) | 0.75 | 1.45 | ||

| (1) | As per the Reserves Report, refer to Reserves Disclosure for additional discussion. |

| (2) | Pro forma Net Debt as at December 31, 2025 is calculated as Net Debt of $88.6 million, adjusted for cash consideration of $62.5 million less the estimated net proceeds under the Equity Offerings of $50.0 million, net of a 4.0% underwriting fee. Net debt, a non-GAAP financial measure, at December 31, 2025 of $88.6 million is unaudited and may change upon finalization of the audited year-end financial statements. “Net Debt” includes bank debt, net of “Adjusted Working Capital”, also a non-GAAP financial measure. Adjusted Working Capital includes cash and cash equivalents, accounts receivable, prepaids and deposits, and accounts payable and accrued liabilities. |

| (3) | The calculation of dilutive proceeds and the fully diluted number of common shares outstanding only includes outstanding securities that are “in-the-money” based on the closing price of Logan common shares of $0.85 per share as at December 31, 2025. |

| (4) | For purposes of the net asset value per share calculation, the Company does not apply the treasury stock-method prescribed by IFRS Accounting Standards. Rather, the fully diluted number of common shares outstanding is determined by adding the total number of outstanding “in-the-money” securities to the number of common shares outstanding at the calculation dates. |

| (5) | Fully diluted common shares outstanding assumes closing of the Equity Offerings for aggregate gross proceeds of $50.0 million. |

Other Measurements

All dollar figures included herein are presented in Canadian dollars, unless otherwise noted. This press release contains various references to the abbreviation "BOE" which means barrels of oil equivalent. Where amounts are expressed on a BOE basis, natural gas volumes have been converted to oil equivalence at six thousand cubic feet (mcf) per barrel (bbl). The term BOE may be misleading, particularly if used in isolation. A BOE conversion ratio of six thousand cubic feet per barrel is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the

wellhead and is significantly different than the value ratio based on the current price of crude oil and natural gas. This conversion factor is an industry accepted norm and is not based on either energy content or current prices. Such abbreviation may be misleading, particularly if used in isolation.

References to "oil" or "crude oil" in this press release include light crude oil, medium crude oil, heavy oil and tight oil combined. NI 51-101 includes condensate within the product type of "natural gas liquids". References to "natural gas liquids" or "NGLs" include pentane, butane, propane and ethane. References to "gas" or "natural gas" relates to conventional natural gas. References to "liquids" includes crude oil, condensate and NGLs. The Company has disclosed "condensate" separately from other natural gas liquids in this press release since the price of condensate as compared to other natural gas liquids is currently significantly higher and the Company believes that this presentation provides a more accurate description of its operations and results.

Estimated ultimate recovery is an approximation of the quantity of oil or gas that is potentially recoverable or has already been recovered from a reserve or well. The reader is cautioned that these amounts may not be directly comparable to other companies, as the term EUR does not have a standardized meaning under IFRS Accounting Standards or NI 51-101.

Share Capital

Common shares of Logan trade on the TSXV under the symbol "LGN".

As of the date hereof, there are 595.7 million Common Shares outstanding. Pro forma completion of the Equity Offerings, there will be 664.2 million Common Shares outstanding. There are no preferred shares or special shares outstanding. Logan's convertible securities outstanding as of the date of this press release include: 64.3 million Common Share purchase warrants with an exercise price of $0.35 per share expiring July 12, 2028; and 42.7 million stock options with an exercise price of $0.78 per share and an average remaining term of 3.4 years.

Forward-Looking and Cautionary Statements

Certain statements contained within this press release constitute forward-looking statements within the meaning of applicable Canadian securities legislation. All statements other than statements of historical fact may be forward-looking statements. Forward-looking statements are often, but not always, identified by the use of words such as "outlook", "anticipate", "budget", "plan", "endeavor", "continue", "estimate", "evaluate", "expect", "forecast", "monitor", "may", "will", "can", "able", "potential", "target", "intend", "consider", "focus", "identify", "use", "utilize", "manage", "maintain", "remain", "result", "cultivate", "could", "should", "believe" and similar expressions (or grammatical variations or negatives thereof). Logan believes that the expectations reflected in such forward-looking statements are reasonable as of the date hereof, but no assurance can be given that such expectations will prove to be correct and such forward-looking statements should not be unduly relied upon. Without limitation, this press release contains forward-looking statements pertaining to: the completion of the Equity Offerings, the expansion of the Company's credit facilities and the Acquisition and the terms and timing thereof (including the use of proceeds from the Equity Offerings); satisfaction or waiver of the closing conditions to the Equity Offerings, the expansion of the Company's credit facilities and the Acquisition and the anticipated Closing Date; receipt of required regulatory and stock exchange approvals for the completion of the Equity Offerings; insider participation in the Equity Offerings; anticipated benefits of the Acquisition, including the impact of the Acquisition and the Acquired Assets on the Company's operations, reserves, inventory and opportunities, financial condition, realized pricing, access to capital and overall strategy (including expectations that the Acquisition will be highly accretive on all key metrics both immediately and in the long term); Logan's revised 2026 guidance and capital budgets and operating plan, including drilling, the business plan, objectives and strategy of Logan and the anticipated results thereof; anticipated revenue, capital and operating cost synergies resulting from the Acquisition; management's tracking record of generating excess return in various business cycles; the Company's opportunity rich assets; the success of the Company's growth plan; the success of the Company's drilling program based on initial results; future drilling plans; and risk management activities, including hedging. Statements relating to reserves, EUR, recovery, costs and valuation are also deemed to be forward looking statements, as they involve the implied assessment, based on certain estimates and assumptions, that the reserves described exist in the quantities predicted and that the reserves can be profitably produced in the future.

The forward-looking statements and information are based on certain key expectations and assumptions made by Logan, including, but not limited to, expectations and assumptions concerning: the receipt of all approvals and satisfaction of all conditions to the completion of the Equity Offerings, the expansion of the Company's credit facilities and the Acquisition, the business plan of Logan, the timing and success of future drilling, development and completion activities and infrastructure projects, the performance of existing wells, the performance of new wells, the availability and performance of facilities and pipelines, the geological characteristics of Logan's properties, the successful integration of the recently acquired assets into Logan's operations, the successful application of drilling, completion and seismic technology, the Company's ability to secure sufficient amounts of water, prevailing weather conditions, prevailing legislation affecting the oil and gas industry, prevailing commodity prices, price volatility, future commodity prices, price differentials and the actual prices received for the Company's products, anticipated fluctuations in foreign exchange and interest rates, impact of inflation on costs, royalty regimes and exchange rates, the application of regulatory and licensing requirements, the availability of capital (including under the Equity Offerings and the Company's expanded credit facilities), labour and services, the creditworthiness of industry partners, general economic conditions, and the ability to source and complete acquisitions.

Although Logan believes that the expectations and assumptions on which such forward-looking statements and information are based are reasonable, undue reliance should not be placed on the forward-looking statements and information because Logan can give no assurance that they will prove to be correct. By its nature, such forward-looking information is subject to various risks and uncertainties, which could cause the actual results and expectations to differ materially from the anticipated results or expectations expressed. These risks and uncertainties include, but are not limited to, counterparty risk to closing the Equity Offerings, the expansion of the Company's credit facilities and the Acquisition, fluctuations and volatility in commodity prices (including pursuant to determinations by the Organization of Petroleum Exporting Countries and other countries (collectively referred to as OPEC+) regarding production levels) and the risk of an extended period of low oil and natural gas prices; changes in industry regulations and legislation (including, but not limited to, tax laws, royalties, and environmental regulations); the imposition or expansion of tariffs imposed by domestic and foreign governments or the imposition of other restrictive trade measures, retaliatory or countermeasures implemented by such governments, including the introduction of regulatory barriers to trade and the potential material adverse effect on the Canadian, U.S. and global economies, and by extension the Canadian oil and natural gas industry and the demand and/or market price for the Company's products and/or otherwise adversely affects the Company; changes in the political landscape both domestically and abroad, wars (including ongoing military actions in the Middle East and between Russia and Ukraine), hostilities (including tensions between the U.S. and Venezuela), civil insurrections, foreign exchange or interest rates, increased operating and capital costs due to inflationary pressures (actual and anticipated), risks associated with the oil and gas industry in general, stock market and financial system volatility, impacts of pandemics, the retention of key management and employees, risks with respect to unplanned third-party pipeline outages and risks relating to inclement and severe weather events and natural disasters, such as fire, drought and flooding, including in respect of safety, asset integrity and shutting-in production. The foregoing list is not exhaustive. Please refer to the MD&A and AIF for discussion of additional risk factors relating to Logan, which can be accessed on its SEDAR+ profile at www.sedarplus.ca. Readers are cautioned not to place undue reliance on this forward-looking information, which is given as of the date hereof, and to not use such forward-looking information for anything other than its intended purpose. Logan undertakes no obligation to update publicly or revise any forward-looking information, whether as a result of new information, future events or otherwise, except as required by law.

This press release contains future-oriented financial information and financial outlook information (collectively, "FOFI") about Logan's revised pro forma budget and guidance for 2026, including with respect to prospective results of operations and production and growth, Logan's 2026 pro forma capital program, budget of $175 to $185 million, guidance and components thereof, including average annual production forecasts of 16,000 to 17,000 BOE/d, average H2 production forecasts of 18,000 to 19,000 BOE/d, Operating Income and Operating Netback, after hedging, Adjusted Funds Flow, AFF per share, operating costs and Capital Expenditures before A&D and Net Debt, including pro forma the completion of the Equity Offerings, the expansion of the Company's credit facilities and the Acquisition, all of which are subject to the same assumptions, risk factors, limitations, and qualifications as set forth in the above paragraphs. FOFI contained in this document was approved by management as of the date of this document and was provided for the purpose of providing further information about Logan's proposed business activities in 2026. Logan and its management believe that FOFI has been prepared on a reasonable basis, reflecting management's best estimates and judgments, and represent, to the best of management's knowledge and opinion, the Company's expected course of action. However, because this information is highly subjective, it should not be relied on as necessarily indicative of future results. Logan disclaims any intention or obligation to update or revise any FOFI contained in this document, whether as a result of new information, future events or otherwise, unless required pursuant to applicable law. Readers are cautioned that the FOFI contained in this document should not be used for purposes other than for which it is disclosed herein. Changes in forecast commodity prices, exchange rates, differences in the timing of capital expenditures, and variances in average production estimates can have a significant impact on the Company's 2026 pro forma guidance. The Company's actual results may differ materially from these estimates.

This press release is not an offer of the securities for sale in the United States. The securities offered have not been, and will not be, registered under the U.S. Securities Act" or any U.S. state securities laws and may not be offered or sold in the United States absent registration or an available exemption from the registration requirement of the U.S. Securities Act and applicable U.S. state securities laws. This press release shall not constitute an offer to sell or the solicitation of an offer to buy, nor shall there be any sale of these securities, in any jurisdiction in which such offer, solicitation or sale would be unlawful.

Neither the TSXV nor its regulation services provider (as that term is defined in the policies of the TSXV) accepts responsibility for the adequacy or accuracy of this news release.

Abbreviations

| A&D | acquisitions and dispositions |

| AECO | Alberta Energy Company "C" Meter Station of the NOVA Pipeline System |

| AIF | refers to the Company's Annual Information Form dated March 19, 2025 |

| bbl | barrel |

| bbls/d | barrels per day |

| bcf | one billion cubic feet |

| BOE | barrels of oil equivalent |

| BOE/d | barrels of oil equivalent per day |

| BTax | before tax |

| CA$ or CAD | Canadian dollar |

| COGEH | the most recent publication of the Canadian Oil and Gas Evaluations Handbook |

| EUR | estimated ultimate recovery |

| GJ | gigajoule |

| H2 | second half of the year or six month period ending December 31 |

| Mbbl | one thousand barrels |

| MBOE | one thousand barrels of oil equivalent |

| mcf | one thousand cubic feet |

| mcf/d | one thousand cubic feet per day |

| MD&A | refers to Management's Discussion and Analysis of the Company dated November 12, 2025 |

| MMbtu | one million British thermal units |

| MMcf | one million cubic feet |

| MMcf/d | one million cubic feet per day |

| MM | millions |

| $MM | millions of dollars |

| MPa | megapascal unit of pressure |

| NAV | net asset value |

| NGL(s) | natural gas liquids |

| NPV | net present value |

| NPV10 | net present value with a discount rate of 10% |

| NI 51-101 | National Instrument 51-101 – Standards of Disclosure for Oil and Gas Activities |

| nm | "not meaningful", generally with reference to a percentage change |

| NYMEX | New York Mercantile Exchange, with reference to the U.S. dollar "Henry Hub" natural gas price index |

| PDP | proved developed producing reserves |

| Reserves Report | the oil and gas reserves evaluation as of December 31, 2025 as prepared by the Company's independent qualified reserves evaluator, McDaniel & Associates Consultants Ltd. |

| TP | total proved reserves |

| TPP | total proved plus probable reserves |

| TSXV | TSX Venture Exchange |

| US$ or USD | United States dollar |

| WTI | West Texas Intermediate, the reference price paid in U.S. dollars at Cushing, Oklahoma for crude oil of standard grade |

A photo accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/ab263418-14cf-4c85-bbd0-e2aa4f9e484f

![]()

Simonette

Simonette image

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.